|

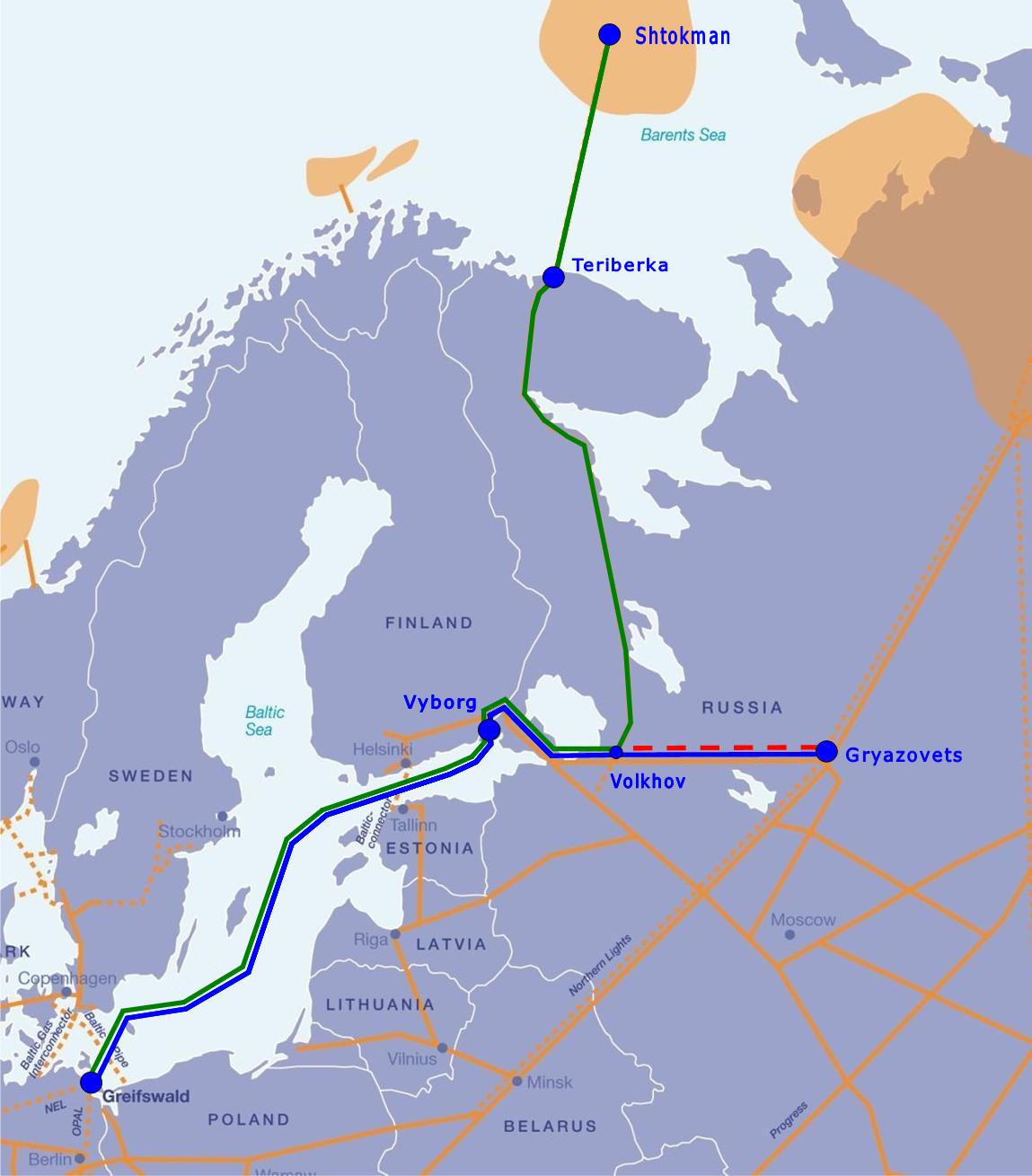

The two-line Nord Stream project

faces a serious synchronization problem. The first line of the new export

project of Gazprom will be fed by the 917-km

Gryazovets-Vyborg

pipeline being built now. The second line is supposed to receive gas from

the Shtokman gas field in the Barents Sea via the 1365-km

Murmansk-Volkhov pipeline (aka Teriberka-Volkhov)scheduled to be

commissioned in 2013.

According to Nord Stream AG,

the second line of the

project is due to be completed in 2012. It is clear that Shtokman will not

start production in 2013. In my view, it is unlikely to be commissioned before

the mid-2020s.

Without additional gas deliveries to

Vyborg, Nord Stream can work at a maximum of 55% of its design capacity, which

means the second line is not needed. Gazprom can solve the bottleneck at Vyborg

by building another 510-km pipeline from Gryazovets to Volkhov. However, this

asset will not be needed when the Teriberka-Volkhov pipeline gets operational.

Gazprom has to chose between laying

an empty 1200-km pipe from Vyborg to Greifswald or building a temporary 510-km

line from Gryazovets to Volkhov. From the financial standpoint, this is a choice

between freezing $6 billion for several years starting from 2012 or $3 bn

forever after the

pipeline from Shtokman is commissioned. In any case, this is a no-win situation

for Gazprom. For Nord Stream, it would be much better if Gazprom builds the

temporary $3-billion line from Gryazovets. At 55% load, Nord Stream would be a

total loss. As a matter of fact, it may be cheaper to abandon the plan of

building the second line of Nord Stream.

Considering the current market

situation, it looks very unlikely for Gazprom to sell any additional gas under

the old pricing formula. Until the 2020s, the Russian gas monopoly is more

likely to export minimum volumes of about 150 bcm/year allowed by the

take-or-pay contracts. Europe will buy additional gas at the price below the

cost of Russian gas delivered to the EU border. In this case, the project

disapproval by the Swedish authorities will be commercially beneficial for

Gazprom. On the other hand, the EU will be more secure with the financially

healthy Gazprom.

Mikhail

Korchemkin

November 4, 2009

Malvern, Pennsylvania,

USA

|