|

Economics of Russian-Ukrainian Gas Conflict:

Summary for Beginners

Questionable benefits

of Gazprom. Deal with Turkmenistan looks like a bluff.

There are many political statements on

financial gains of Gazprom and Russia after the raise of gas price for

Ukraine. We believe these hopes are groundless.

To begin with, Gazprom is not selling gas

to Ukraine since 1998. Before 1998, Gazprom had two categories of gas

transactions with Ukraine: (1) “free” gas delivered as payment for transit

services, and (2) export gas that supposed to be paid for. Deliveries of

“free” gas and export gas in one package created many opportunities for grey

schemes. According to Gazprom, only 38% of Ukrainian gas bills were paid.

From 1998, Gazprom is delivering only “free”

gas in payment for transit services. Export flows were handled first by “Itera”,

then by “Eural Trans Gas” and finally by “RosUkrEnergo”. The separation of

“free” gas from export gas has unveiled illegal off-takes, which were

formerly hidden in the flows of “free” gas. Remarkably, both Gazprom and

“Itera” gained from the separation of gas flows. Gazprom has eliminated the

problem of collecting money from bad clients and got additional revenues

from sales of gas transportation services. “Itera” took the cream of

Ukrainian market by selling gas only to the most reliable clients.

Gazprom was steadily decreasing the volumes of

payment gas from 30 bcm in the late 1990s to 26 bcm in 2004 and 21 bcm in

2005 (bcm = billion cubic meters). Specific volumes were negotiated between

the gas monopolies of Russia and Ukraine. From 1998, the parties used gas

price of $50/mcm and transit

tariff of $1.0937/mcm per 100 km (mcm = thousand cubic meters). Under these terms, transit expense of

Gazprom was roughly equal to the gas procurement expense of Ukraine. There

were no cash sales until 2004, when Gazprom exported additional 6 bcm at

$80/mcm as compensation for the re-exports of “RosUkrEnergo”. The reasons

for these re-exports and transfer of Gazprom’s profits to Switzerland are

unclear. However, re-export of “RosUkrEnergo” is the only reason for

additional sales of Gazprom to Ukraine. We expect these re-exports to stop

and do not take them into account.

As of late 2005, Gazprom is not receiving

any money for gas delivered to Ukraine and is paid in kind by transit

service. Turkmenistan is exporting gas to Ukraine for cash with

“RosUkrEnergo” acting as a broker.

Now Gazprom wants to raise the price of gas

for Ukraine from $50 to $230/mcm. Benefits of this step are doubtful, but

losses are obvious.

If Gazprom plans to sell the same 21

bcm at $230/mcm and pay just a share of revenue for transit service,

the management of Russian gas monopoly is very likely to be disappointed.

Ukrainian NAK “Naftogaz” can raise the transit tariff and introduce a

“European” tariff for the reservation of gas storage capacity. Formally,

Gazprom is not using the storage facilities now under the special low-cost

transit agreement. In reality, Ukrainian storage facilities provide the

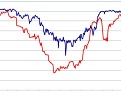

export flow of Russian gas to Europe in winter. The difference between

export flows in winter and summer is about 100 million cubic meters a day,

while the gas flow to Ukraine is roughly the same through the year (see

chart). Gazprom

needs Ukrainian storage capacity more than NAK “Naftogaz” does. When the

transit terms change, Gazprom would have to pay for storage. In Europe,

storage capacity reservation for a year can cost anything from €100-150 per

one cubic meter per hour.

If Gazprom plans to sell more gas to

Ukraine, it should squeeze Turkmenistan out of

the market. The deal between Gazprom and Turkmenistan concluded on

December 29, 2005 looks like the move in this direction indeed. Gazprom

reports that it buys 15 bcm of Turkmen gas in the first quarter of 2006.

Actually, this is exactly the combined capacity of all pipelines running

from Turkmenistan to Russia, which means no other gas, including from

Uzbekistan and Kazakhstan, is getting through.

Moreover, a simple

analysis of

the gas balance of Turkmenistan indicates that the new agreement

is a bluff. In January-March 2006, Turkmenistan is capable to

produce about 6.0 bcm a month, at least 1.5 bcm/month of which should go for

domestic consumption. Exports to Iran take another 0.5 bcm/month. There

is no 15 bcm of Turkmen gas available for Gazprom in the first quarter of

2006.

We

advice to wait until Turkmenbashi confirms the volumetric and pricing

details of Gazprom's statement. There

is also something wrong with Gazprom buying Turkmen gas at

$85-$90 at the Russian border ($65 at the border of Turkmenistan) and reselling it to Ukraine at $230/mcm. Turkmenbashi is not that simple person. However, even such a profitable

resale would bring Gazprom a big total loss compared with the terms of 2005

(Table 1). The loss is bigger

if Turkmenistan gets its fair share, or if Ukraine

raises its transit tariff to the level paid by Gazprom in Bulgaria or

Austria. The tariff for reservation of Ukrainian storage capacity also has

space for an increase. In addition, Gazprom would

need to ban exports of Russian independent gas producers to Ukraine, because

the independents can offer much lower price than $230/mcm.

Table 1. Comparison

of Revenues and Expenses of Gazprom

|

Unit

|

$60/mcm

|

$230/mcm

|

| Ukrainian

transit expense: |

|

|

|

Volume of payment gas

|

bcm

|

26

|

26

|

Value of payment gas

|

$ billion

|

1.6

|

6.0

|

Ukrainian transit tariff

|

$/mcm/100km

|

1.09

|

3.00

|

Storage capacity reservation tariff

|

$/cub.m/hour/a

|

-

|

150.00

|

Payment in kind (by gas) for transit service

|

$ billion

|

(1.6)

|

-

|

Revenue from gas sale

|

$ billion

|

1.6

|

6.0

|

Cash payment for transit services

|

$ billion

|

-

|

(4.3)

|

Cash payment for storage reservation

|

$ billion

|

-

|

(2.1)

|

Total cash payment to Ukraine

|

$ billion

|

-

|

(6.4)

|

Export duty - 30%

|

$ billion

|

(0.5)

|

(1.8)

|

Total transit expense of Gazprom:

|

$ billion

|

(0.5)

|

(2.2)

|

|

Transit revenue: |

|

|

|

Transit volume from Turkmenistan

|

bcm

|

34

|

-

|

Transit tariff of Gazprom

|

$/mcm/100km

|

1.09

|

3.00

|

Transit revenue:

|

$ billion

|

0.3

|

-

|

|

Resale

of Turkmen gas: |

|

|

|

Volume of gas

|

bcm

|

-

|

34

|

Cost at the Russian border

|

$/mcm

|

64

|

90

|

Import duty - 5%

|

$/mcm

|

-

|

5

|

Total Gazprom expense at the Russian border

|

$ billion

|

-

|

(3.2)

|

Gross revenue from resale to Ukraine

|

$ billion

|

-

|

7.8

|

Turkmenistan share in profits - 25%

|

$ billion

|

-

|

(1.2)

|

Export duty - 30%

|

$ billion

|

-

|

(2.3)

|

|

|

$ billion

|

-

|

1.1

|

Total net result of Gazprom:

|

$

billion

|

(0.2)

|

(1.1)

|

In best case, Gazprom is likely to supply 60

bcm and spend the major share of revenue on transit service and reservation of

storage capacity in Ukraine. The transit expense will go up and profits

from exports to Europe will decrease. Note that additional export duties

(30% of $230/mcm) will exceed $3.6 billion a year. In the most favorable

case, Gazprom loses over billion dollars a year.

NAK "Naftogaz Ukraine" gets 60 bcm of gas at

net cost of $7.4 billion. This transfers into the average Ukrainian internal

price of $124/mcm. The most favorable case for Gazprom means the worst case

for Ukraine, so the average Ukrainian price may be lower than $124/mcm.

We must note that

Ukraine has more other options for an adequate response to price raise.

However, packaging of gas transit issues with other political matters is

inappropriate from our point of view.

At the first glance, the Russian state looks

like a sure winner in this game. Indeed, the tax collection increases,

though the increase is cut by the lower profit tax of Gazprom.

However, the state is likely to lose as the

main shareholder of Gazprom. In the context of growing gas price in

Europe, the capitalization of Gazprom could have been higher under different

terms of Ukrainian transit.

We have made preliminary comparison of net

present value of additional tax income of the state and NPV of lost cash

flow of Gazprom. The state loses if the price is below $220/mcm and gains if

the price is higher. The break-even price is substantially higher if

additional measures of Ukraine and effects of probable increase of price of

gas from Uzbekistan and Kazakhstan are taken into account. The calculations

were done before the announcement of new deal with Turkmenistan. The

agreement with Turkmenistan increases the gain of the Russian state

because of the huge increase of export duties' collection from Gazprom.

Unlike the Russian state, minority

shareholders of Gazprom will just lose. The loss may not be noticed while

the European gas price is growing. However, the shareholders are likely to

understand that the main goal of Gazprom is not the profit maximization, but

rather tax maximization and fulfillment of political goals of the current

presidential administration.

Mikhail Korchemkin

December 29, 2005 (updated on December 30, 2005)

Previous publications on

Russian-Ukrainian gas dispute:

Russian-Ukrainian Gas Conflict: Financial

Effects of the Russian Side

- 2

Russian-Ukrainian Gas Conflict: Financial Effects of the

Russian Side

Brief

history of Soviet and Russian gas pipeline policy

Clarifying

the math of Ukrainian transit tariff

|